You are ready to embark on a digital transformation journey with your bank, and you want digital and mobile account opening. However, you are hesitant, because everyone tells you that you can’t do it while using your legacy core system. That it is like “putting new wheels on an old car”. That is not true. There are many community banks that have successfully launched digital account opening, while using the core system of one of the big three providers (Jack Henry, FIS or Fiserv). Read on, you may save yourself a lot of time and money.

How can I launch digital account opening on a legacy core?

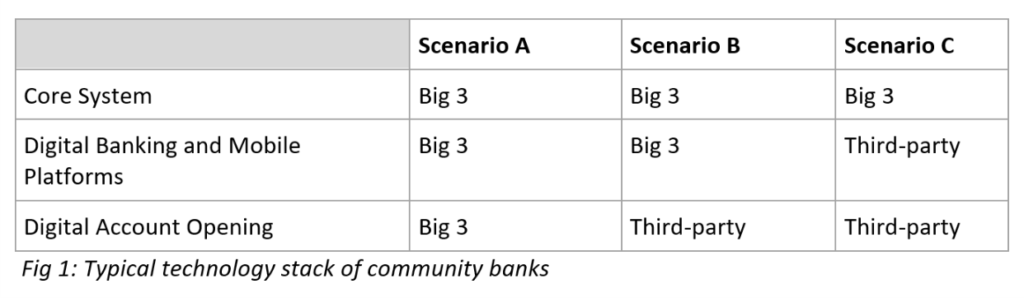

There are many permutations, but by far most banks that launched digital account opening, fall into one of the three technology stack scenarios described below:

A. Core system from legacy provider, digital banking platform from legacy provider, digital account opening from legacy provider.

B. Core system from legacy provider, digital banking platform from legacy provider, digital account opening from third-party provider.

C. Core system from legacy provider, digital banking platform from third party provider, digital account opening from third-party provider.

As you can see from figure 1 (above), the general trend is to retain the legacy core provider.

Keep it simple

Let me clarify, there are some great third-party digital banking and digital account opening vendors out there, and sometimes it makes sense to go with them. They are often at the forefront of innovation and may be a great fit for your bank. There are many successful examples of that, to which I can testify.

However, the broader point that I am trying to bring across, is that you could also execute on a digital strategy, by keeping things simple and minimizing disruption. In fact, you may potentially run a bigger execution risk if you are changing strategy and your core system at the same time.

The digital banking and digital account opening platforms of the Big 3 may not always have the latest bells and whistles, but are well tested and integrates seamlessly with their core. As I have stated in previous articles, it is not about how fancy your technology is, it is more about how you string it all together and how you blend it with your existing operational and service strengths.

Like most banks, you have budget and talent constraints. Digital and mobile account opening is a process that involves more than just choosing a good vendor. It involves figuring out how to grow your business cost effectively through your new origination channel. It also requires a fresh look at the risk management around deposit accounts and online transfers. You may want to work with a consultant that has done it before to learn about best practices and learn from the mistakes of others.

Successful examples

One of the most successful digital bank brands in the US runs on a Jack Henry core system. A small community bank in the Midwest runs a well-known standalone internet brand, using the same legacy core system for both the branches and the online brand. There are many more successful examples, but how you stack your technology, is a unique decision for every bank.

No matter how much community banks look the same from the outside, each has its own challenges and opportunities with digital transformation. And each needs to be evaluated, not just on proposed strategy, but also on existing strengths and resources. What is an undisputed fact though, is that that digital transformation and digital account opening (also mobile) is not a “nice to have” anymore, it is a strategic imperative.

Community banking and digital banking are not mutually exclusive. In fact, combined, they provide the best of both worlds, allowing community banks to compete against the mega banks, without abandoning their relationship driven mission. You can do both, blending the existing well-proven business model of your community bank, with the changing customer expectations of digital delivery, while improving your bottom line in the process. Ensuring that your customers don’t open their next account online at a competitor.

About:

Adriaan van Zyl is the CEO at BankINNOVATE.com. He is a leading Digital Banking and FinTech expert, actively engaged in guiding banks through Digital Banking Transformation, as well as the establishment and managing of Bank/FinTech partnerships. Helping community banks to implement cost effective Digital and Mobile Account Opening technology and processes, and with the evaluation and selection of Online & Mobile Banking platforms. Visit bankINNOVATE.com for more information.